Insights + Resources

Epic Insights

Understanding Risk

Jul 9, 2025

Few terms in personal finance are as important, or used as frequently, as “risk.” Nevertheless, few terms are as imprecisely defined. Generally, when financial advisors or the media talk about investment risk, their focus is on the historical price volatility of the asset or investment under discussion.

Few terms in personal finance are as important, or used as frequently, as “risk.” Nevertheless, few terms are as imprecisely defined. Generally, when financial advisors or the media talk about investment risk, their focus is on the historical price volatility of the asset or investment under discussion.Tags: charlotte NC, financial advisor, financial advisor charlotte nc, Financial Help, Financial Planner Charlotte NC, Retirement Planning, Risk Management

Market Update – America Gets Record High Stock Prices for Its Birthday

Jul 7, 2025

As Americans get their grills and beach chairs ready for the July 4th holiday, the stock market and the weather across much of the country have both been on heaters. Stocks and bonds continue to effectively navigate a complex policy landscape shaped by evolving trade dynamics, geopolitical tensions, and fiscal stimulus. The market’s resilience in the face of these crosscurrents has been impressive, proving yet again that the fundamentals of the U.S. economy and corporate America can withstand a lot.

As Americans get their grills and beach chairs ready for the July 4th holiday, the stock market and the weather across much of the country have both been on heaters. Stocks and bonds continue to effectively navigate a complex policy landscape shaped by evolving trade dynamics, geopolitical tensions, and fiscal stimulus. The market’s resilience in the face of these crosscurrents has been impressive, proving yet again that the fundamentals of the U.S. economy and corporate America can withstand a lot.

Tags: Current Events

Retirement Planning Birthday Milestones

Jun 20, 2025

Birthdays may seem less important as you grow older. They may not offer the impact of watershed moments such as getting a driver’s license at 16 and voting at 18. But beginning at age 50, there are several key birthdays that can affect your tax situation, health-care eligibility, and retirement benefits.

Birthdays may seem less important as you grow older. They may not offer the impact of watershed moments such as getting a driver’s license at 16 and voting at 18. But beginning at age 50, there are several key birthdays that can affect your tax situation, health-care eligibility, and retirement benefits.Tags: Retirement Planning

Why Long Term Investing Beats Selling in Volatile Times

Jun 18, 2025

During times like these when geopolitical headlines can be unsettling for investors, we at LPL Research like to remind ourselves of one of our key investing principles. Markets have always faced challenges —ranging from geopolitical conflicts and economic downturns to natural disasters, political upheaval and health crises. These events often trigger short-term volatility and shake investor confidence. However, historical data shows that stock markets have demonstrated a tendency to comeback after each crisis and rise over the longer time horizons. This patten underscores the importance, for strategic investors, of maintaining a long-term perspective – even when the near term outlook feels very uncertain.

Tags: Current Events

Charitable Lead Trusts

Jun 16, 2025

Are you concerned about the inheritance taxes your heirs may have to pay? Then you may want to consider creating charitable lead trusts. (more…)

Tags: Estate Planning, Family Wealth, Financial Planning, Legacy, Wealth Building

Estate Planning – Protecting Your Assets

Jun 9, 2025

You’re beginning to accumulate substantial wealth, but you worry about protecting it from future potential creditors. Whether your concern is for your personal assets or your business, various tools exist to keep your property safe from tax collectors, accident victims, health-care providers, credit card issuers, business creditors, and creditors of others.

Estimating Your Retirement Income Needs

Jun 6, 2025

You know how important it is to plan for your retirement, but where do you begin? One of your first steps should be to estimate how much income you’ll need to fund your retirement. That’s not as easy as it sounds, because retirement planning is not an exact science. Your specific needs depend on your goals and many other factors.

You know how important it is to plan for your retirement, but where do you begin? One of your first steps should be to estimate how much income you’ll need to fund your retirement. That’s not as easy as it sounds, because retirement planning is not an exact science. Your specific needs depend on your goals and many other factors.See More >

Resources

Outlook 2025

2025 Annual Limits for Financial Planning

Outlook 2024

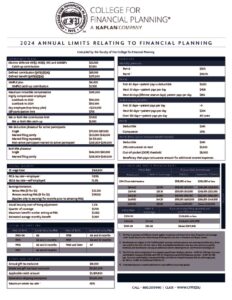

2024 Annual Limits for Financial Planning

Services

Epic Capital provides the following comprehensive financial planning and investment management services: Learn More >

Find us on:

Copyright © 2025 Epic Capital Wealth Management. All Rights Reserved.

Securities offered through LPL Financial. Member FINRA/SIPC.

The LPL Financial representative associated with this website may discuss and/or transact securities business only with residents of the following states: CA, CO, DC, DE, FL, GA, IN, LA, MD, MO, MS, NC, NJ, NY, PA, SC, TN, TX, VA, VT, WA.